The Main Principles Of What Does Recast Mean For Mortgages

The present due date for home mortgage payment holiday applications, which permit house owners to postpone payments for up to six months, is 31 January 2021. You can discover more with the following short articles: For the most recent updates and suggestions, go to the Which? coronavirus information center. Picking the best type of home loan could save you countless pounds, so it's truly essential to understand how they work.

This rate can be repaired (ensured not to change) or variable (might increase or Discover more decrease). View our brief video listed below for a fast description of each various kind of home mortgage and how they work. We discuss them in more information even more down the page. Listed below, you can learn how each mortgage type works, then compare the pros and cons of fixed-rate, tracker and discount rate mortgages in our table.

However, there are a little number of 'life time' trackers where your home mortgage rate will track the Bank of England base rate for the whole mortgage term. When we surveyed home mortgage consumers in September 2019, one in 10 stated they had tracker home loans. With a discount mortgage, you pay the lending institution's standard variable rate (a rate chosen by the lending institution that does not alter very typically), with a fixed quantity discounted.

5% discount rate, you 'd pay 2. 5%. Reduced offers can be 'stepped'; for example, you might take out a three-year deal however pay one rate for 6 months and after that a greater rate for the remaining two-and-a-half years. Some variable rates have a 'collar' a rate listed below which they can't fall or are topped at a rate that they can't exceed.

The Ultimate Guide To How Do Reverse Mortgages Get Foreclosed Homes

Some 5% of those we surveyed in 2019 said they had discount mortgages. With fixed-rate home loans, you pay the very same rate of interest for the whole offer period, no matter interest rate changes elsewhere. Two- and five-year deal periods are the most common, and when you reach the end of your set term you'll generally be proceeded to your loan provider's standard variable rate (SVR).

Fixed-rate mortgages were the most popular in our 2019 home loans study, with six in 10 stating they had one. Five-year deals were the most popular, followed by two-year deals. Each loan provider has its own standard variable rate (SVR) that it can set at whatever level it desires meaning that it's not straight connected to the Bank of England base rate.

72%, according to Moneyfacts. This is greater than many home loan deals presently on the market, so if you're currently on an SVR, it deserves searching for a brand-new home loan. Lenders can change their SVR at any time, so if you're currently on an SVR home mortgage, your payments might possibly increase - specifically if there are rumours of the Bank of England base rate increasing in the future - who provides most mortgages in 42211.

The majority of these had actually had their home loans for more than 5 years. Pros and cons of various mortgage types Throughout the offer period, your rate of interest will not increase, no matter what's taking place to the wider market - after my second mortgages 6 month grace period then what. A good choice for those on a tight budget plan who desire the stability of a repaired monthly payment.

2. 9% If the base rate decreases, your regular monthly repayments will normally drop too (unless your offer has actually a collar set at the existing rate). Your interest rate is only affected by modifications in the Bank of England base rate, not modifications to your lending institution's SVR. You will not know for certain how much your payments are going to be throughout the offer period.

The What Bank Keeps Its Own Mortgages Diaries

2. 47% Your rate will stay listed below your lending institution's SVR for the duration of the deal. When SVRs are low, your discount rate mortgage might have a really inexpensive rate of interest. Your lender might change their SVR at any time, so your repayments could end up being more expensive. 2. 84% * Typical rates according to Moneyfacts.

Whether you should go for a fixed or variable-rate mortgage will depend on whether: You think your income is most likely to change You prefer to understand precisely what you'll be paying monthly You could manage if your monthly payments went up When you take out a home mortgage it will either be an interest-free or repayment home loan, although sometimes individuals can have a combination.

With a payment home mortgage, which is without a doubt the more typical kind of home mortgage, you'll settle a little bit of the loan in addition to some interest as part of each month-to-month payment. Often your scenarios will suggest that you require a particular kind of home mortgage. Kinds of specialist mortgage might include: Bad credit home loans: if you have black marks on your credit rating, there might still be home loans readily available to you - but not from every lender.

Guarantor home mortgages: if you need help getting onto the home ladder, a parent or relative might ensure your loan. Versatile mortgages let you over and underpay, take payment holidays and make lump-sum withdrawals. This indicates you might pay your mortgage off early and save money on interest. You don't typically have to have a special home mortgage to overpay, though; numerous 'typical' deals will also allow you to pay off additional, up to a particular amount usually approximately 10% each year.

Versatile offers can be more expensive than traditional ones, so make sure you will really use their features prior to taking one out. Some home mortgage offers offer you cash back when you take them out. But while the costs of moving can make a heap of cash sound very appealing, these offers aren't always the least expensive as soon as you've factored in fees and interest.

How Many Va Mortgages Can You Have - An Overview

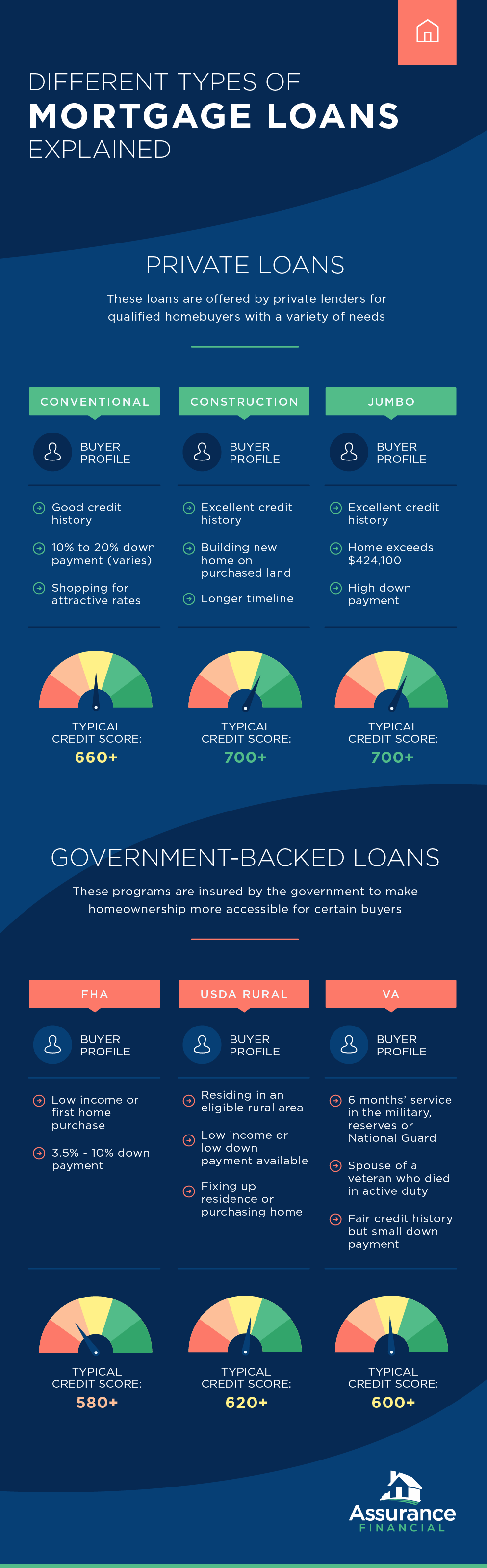

When I was a little girl, there were three home mortgage loan types offered to a house buyer. Buyers could get a fixed-rate traditional mortgage, an FHA loan, or a VA loan. Times have definitely changed. Now there are a dizzying selection of mortgage loan types available-- as the stating goes: more mortgage types than you can shake a stick at! This is the granddaddy of them all.

FHA home mortgage loan types are guaranteed by the federal government through home loan insurance that is funded into the loan. Novice homebuyers are ideal prospects for an FHA loan since the deposit requirements are minimal and FICO ratings do not matter. The VA loan is a government loan is available to veterans who have served in the U.S.

The requirements differ depending upon the year of service and whether the discharge was honorable or wrong. The primary benefit of a VA loan is the customer does not need a down payment. The loan is ensured by the Department of Veterans Affairs however moneyed by a traditional lender. USDA loans are used through the U.S.